Navigating the New Service Tax Landscape

Published:

The amendments to Malaysia’s Service Tax framework, coming into effect on 1 July 2025, are expected to have a nuanced impact on both consumers and businesses. While the government aims to implement a targeted approach that minimizes the burden on the majority of Malaysian citizens, several sectors will likely experience price changes—either directly through new service taxes or indirectly through increased business costs that get passed on to end-users.

Impact of Malaysia’s 2025 Service Tax Amendments

Effective Date: 1 July 2025

Impact on Malaysian Citizens (Consumers)

Certain services will now be directly taxed, leading to noticeable cost increases for specific consumer groups. For instance, although Malaysian citizens are exempted from service tax on private healthcare, traditional and complementary medicine, and allied health services, non-citizens accessing these services will face a 6% service tax. This is expected to affect segments such as medical tourists and expatriates.

In private education, citizens with a valid Kad OKU will be exempt from the 6% tax, offering targeted relief. However, private education services from pre-school to post-secondary levels will be subject to a 6% service tax if annual fees exceed RM60,000 per student. This will increase costs for families sending children to high-end private schools. Additionally, higher education and language centers catering to non-citizens will be taxed, potentially raising costs for international students.

The introduction of an 8% service tax on the rental or leasing of tangible assets (Group K) could indirectly impact consumers. While housing accommodation, including SOHO units and serviced apartments, is excluded, businesses that lease commercial properties may transfer increased rental costs to consumers through higher prices for goods and services.

Construction services for non-residential buildings (Group L) will also see a 6% service tax applied, potentially increasing costs for new commercial and industrial developments. Over time, these cost increases may be passed on to consumers as businesses adjust their pricing strategies to maintain margins.

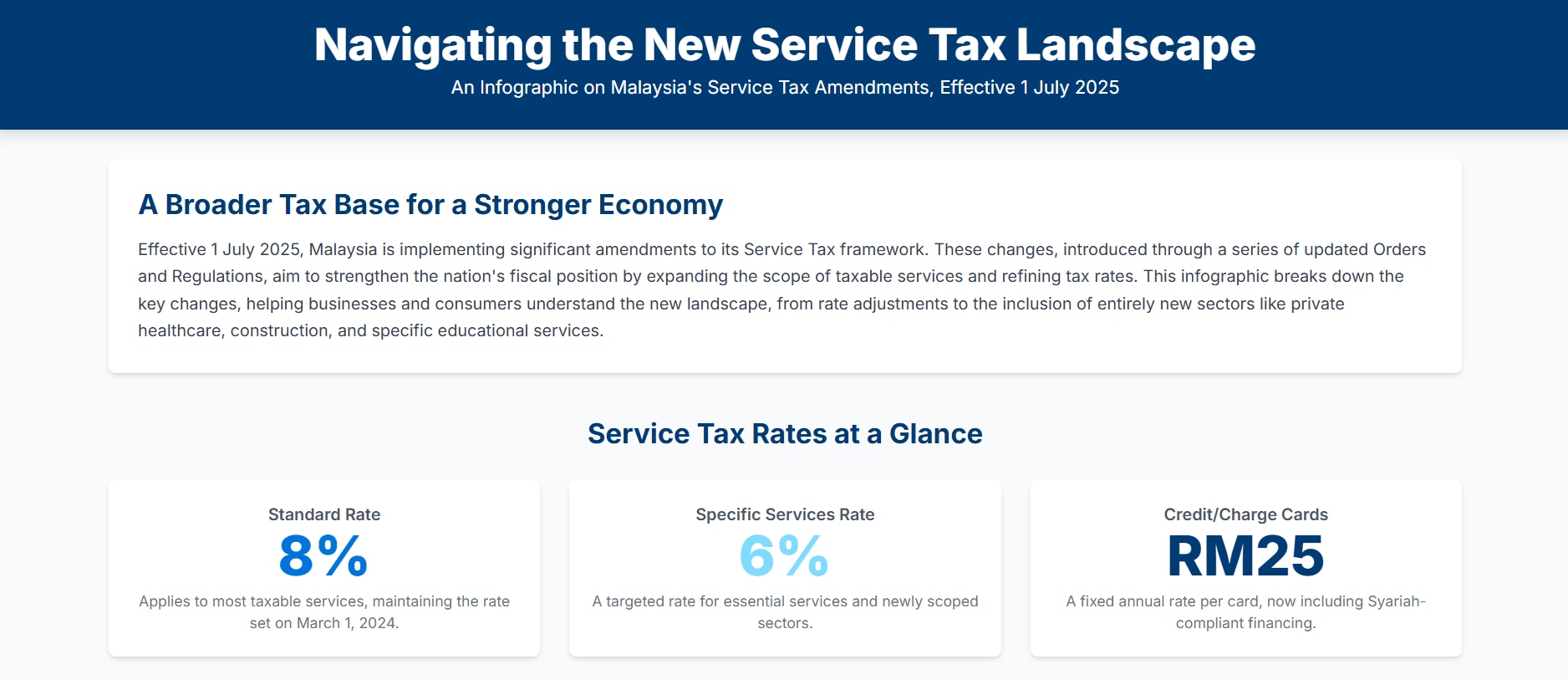

Financial services will be affected through an 8% service tax applied to fee- or commission-based transactions under Group H. Although basic banking services and interest-based transactions are excluded, consumers may face slightly higher charges for other financial services. The RM25 annual tax on credit and charge cards remains unchanged.

Beyond direct taxation, there is a broader concern around cascading effects that may raise the general cost of living. Even with exemptions for business-to-business (B2B) transactions in areas like rental/leasing and construction, the tax paid on inputs—such as rented warehouses or new factory construction—may eventually be embedded into the prices of goods and services. This means that consumers could experience price increases even for items or services not directly taxed under the new rules.

The government has included targeted protections to cushion the impact for vulnerable groups. For example, Malaysian citizens continue to enjoy exemptions for critical services like healthcare and traditional medicine. Additionally, the exemption granted to OKU card holders in education represents a thoughtful effort to reduce the financial burden on persons with disabilities.

Impact on Businesses

The amended service tax regime will raise operating costs for many businesses. Companies consuming newly taxed services—such as leasing machinery, renting commercial properties, or contracting non-residential construction—will see an uptick in input costs. These added expenses may affect profit margins and pricing strategies across industries.

A new layer of compliance will also be required. Businesses that were previously outside the scope of the Service Tax—such as private healthcare providers, construction firms, leasing companies, and some educational institutions—must now register for SST. This involves implementing new accounting systems, updating invoicing procedures, and meeting reporting obligations. Fortunately, a grace period until 31 December 2025 will allow businesses time to adjust without penalty, provided they demonstrate genuine efforts to comply.

From a pricing standpoint, businesses will be forced to choose between absorbing the cost increases or passing them on to customers. The former option may erode margins, especially for SMEs, while the latter could lead to higher consumer prices. Some businesses, especially those locked into non-reviewable contracts signed before July 1, 2025, may be unable to adjust prices, resulting in potential financial losses.

Competitive dynamics could also shift, particularly in sectors where only certain segments are taxed. For example, high-fee private education providers and healthcare facilities serving non-citizens may become less attractive compared to untaxed or international alternatives. This could impact enrollment, revenue, and long-term viability.

One bright spot for businesses is the availability of B2B exemptions, particularly for Groups K and L (Rental/Leasing and Construction Works). These exemptions help reduce the risk of double taxation within supply chains, allowing some businesses to maintain cost competitiveness. However, they don’t eliminate all cascading effects and must be strategically managed.

Summary

In conclusion, the 2025 amendments to Malaysia’s Service Tax framework represent a significant policy shift aimed at broadening the tax base and increasing government revenue. For citizens, essential services such as healthcare and education have been safeguarded through well-targeted exemptions. However, indirect price increases are likely as businesses adjust to new costs. For businesses, the amendments introduce both financial and administrative challenges, requiring careful planning and strategic decision-making. Overall, the changes will prompt a recalibration of pricing models, contract structures, and compliance processes across sectors.